UAE Corporate Tax Law

Chapter 5 of the UAE Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses (‘the CT Law’) provides for ‘Free Zone Person outlines specific provisions concerning the taxation of Free Zone Person effective from tax periods starting on or after 01 June 2023.

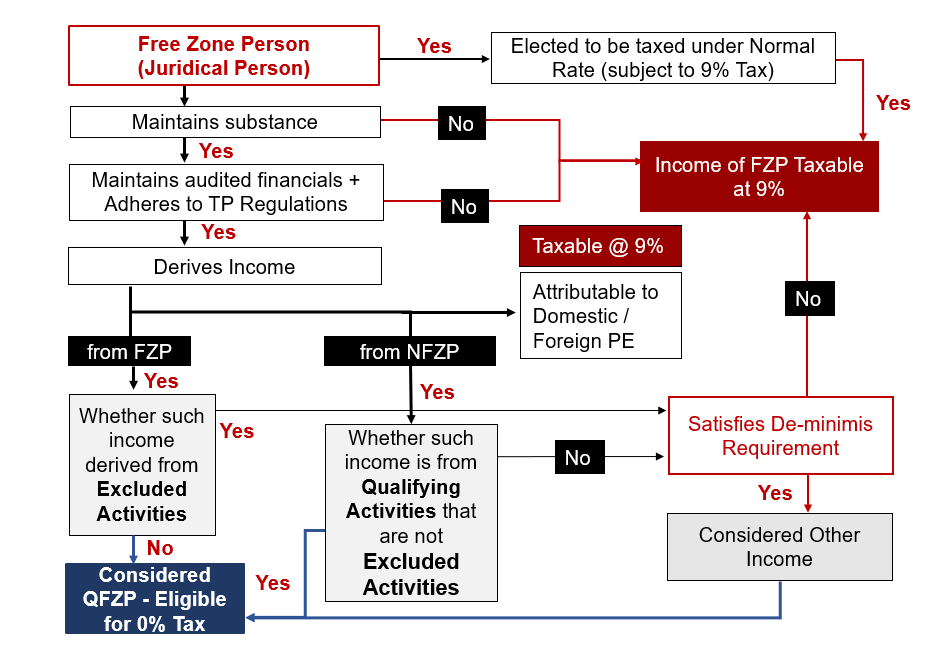

Article 3 of the CT Law establishes the tax rates applicable to Qualifying Free Zone Persons (‘QFZP’). A Corporate Tax rate of 0% (Zero percent) is imposed on their Qualifying Income, while a rate of 9% (Nine percent) is applied to their Taxable Income that is not Qualifying Income

To comprehend the applicability of the CT Law to Free Zones, it is crucial to understand key terms as defined in Article 1 of the CT Law. These terms include "Free Zone," "Free Zone Person," "Qualifying Income," and "Qualifying Free Zone Person." A Free Zone Person is a juridical person incorporated, established or otherwise registered in a Free Zone, including a branch of a Non-Resident Person registered in a Free Zone must satisfy the conditions outlined in Article 18 to be classified as a QFZP. Furthermore, to benefit from the tax advantage of a 0% rate, the QFZP must generate Qualifying income.

Article 18 of the CT law describes that a QFZP is a Free Zone Person that meets all of the following conditions:

- Maintains adequate substance in the State.

- Derives Qualifying Income as specified in a decision issued by the Cabinet at the suggestion of the Minister.

- Has not elected to be subject to Corporate Tax under Article 19 of this Decree-Law.

- Complies with the requirements of TP Compliances as per Article 34 (Arm’s Length Principle) & Article 55 (Documentation).

- Meets any other conditions as may be prescribed by the Minister.

On 01 June 2023, the Ministry of Finance (‘MoF’) issued two decisions i.e. Cabinet Decision No. 55 and Ministerial Decision No. 139 of 2023 available at https://mof.gov.ae/tax-legislation/ provide detailed information regarding the determination of Qualifying Income for QFZP, as well as outline the activities categorized as Qualifying Activities and Excluded Activities.

KEY FEATURES:

Additional Conditions:

In addition to Article 18 of CT Law, a Qualifying Free Zone Person needs to meet the below two additional requirements:

- Its Non-Qualifying revenue does not exceed the De Minimis requirement (lower of 5 million or 5% of total revenue)

- It prepares and maintains Audited Financial Statements

Adequate Substance:

- The Free Zone person undertakes Core Income Generating Activities (CIGA) in the free zone

- The activities carried out by the Free Zone Person must have

- Adequate assets

- Adequate number of qualified employees

- Adequate operating expenditure is incurred

(The above activities can be outsourced to related party or third party in Free Zone provided it is supervised by the QFZP)

Qualifying Income:

- Income derived from transactions with other Free Zone Persons, except for income derived from “Excluded Activities”.

- Income derived from transactions with a Non-Free Zone Person, but only in respect of "Qualifying Activities" that are not Excluded Activities.

- Any other income provided that the QFZP satisfies the de minimis requirements.

Excluded Activities include the following:

- Transactions with natural persons (subject to certain exceptions under Qualifying Activities related to shipping and aircrafts, fund, wealth and investment management);

- Regulated banking, finance, leasing and insurance activities;

- Ownership or exploitation of intellectual property assets, and

- Ownership or exploitation of immovable property, except for transactions with Free Zone Persons in relation to commercial property located in a Free Zone.

- Ancillary activities to the above mentioned activities

Qualifying Activities include the following:

- Manufacturing and processing of goods or materials;

- Holding of shares and other securities;

- Ownership and operation of ships;

- Regulated reinsurance and fund /wealth management;

- Headquarter, Treasury and financing services to related parties;

- Financing and leasing of aircraft

- Logistics services

- The distribution of goods in or from a designated zone subject to certain conditions.

- Ancillary activities to the above mentioned activities

De Minimis Requirements:

The de minimis requirements will be satisfied where non-qualifying Revenue does not exceed 5% of total revenue or AED5,000,000, whichever is lower.

Non-qualifying Revenue is revenue derived from Excluded Activities or activities that are not Qualifying Activities where the other party is a non-Free Zone Person.

A visual representation illustrating the decisions can be described as follows:

Key Takeaway & Way Forward:

- "Free Zone Person" specifically refers to juridical persons within the Free Zone. Natural persons conducting business in the UAE and juridical persons outside the Free Zone are not considered Free Zone Persons.

- Meeting the specific conditions to qualify as a QFZP is crucial. A thorough analysis of these conditions is necessary, as failure to meet them during a Tax Period would result in disqualification as a QFZP for the subsequent four Tax Periods.

- Free Zone entities should understand the distinction between Qualifying activities, which may make them eligible for tax benefits, and Excluded activities, which may not qualify for such benefits. Aligning business activities with the provisions of the CT Law will help determine qualification and make informed decisions about tax status and potential benefits.

- Separate books of accounts should be maintained for Domestic Permanent Establishment/Foreign Permanent Establishment.

- Transactions with natural persons may not be considered Qualified Income except transaction in relation to shipping and aircrafts, fund, wealth and investment management as mentioned in Qualifying activities.

- Reviewing transactions related to immovable property is necessary to determine tax implication on income earned from such immovable property.

- According to FAQs released by the MoF, QFZPs that are part of multinational groups are expected to be subject to a different Corporate Tax rate once the OECD Pillar Two rules are incorporated into the UAE CT regime.

Feel free to reach us to resolve your queries regarding the Taxability of a Free Zone person under UAE CT Law.

Purvi Mehta

Manager- Direct Tax

M: +971 52 2500480

E: purvi@emiratesca.com